A Survey of Myanmar's Socioeconomic Crisis and Public Resilience

Summary

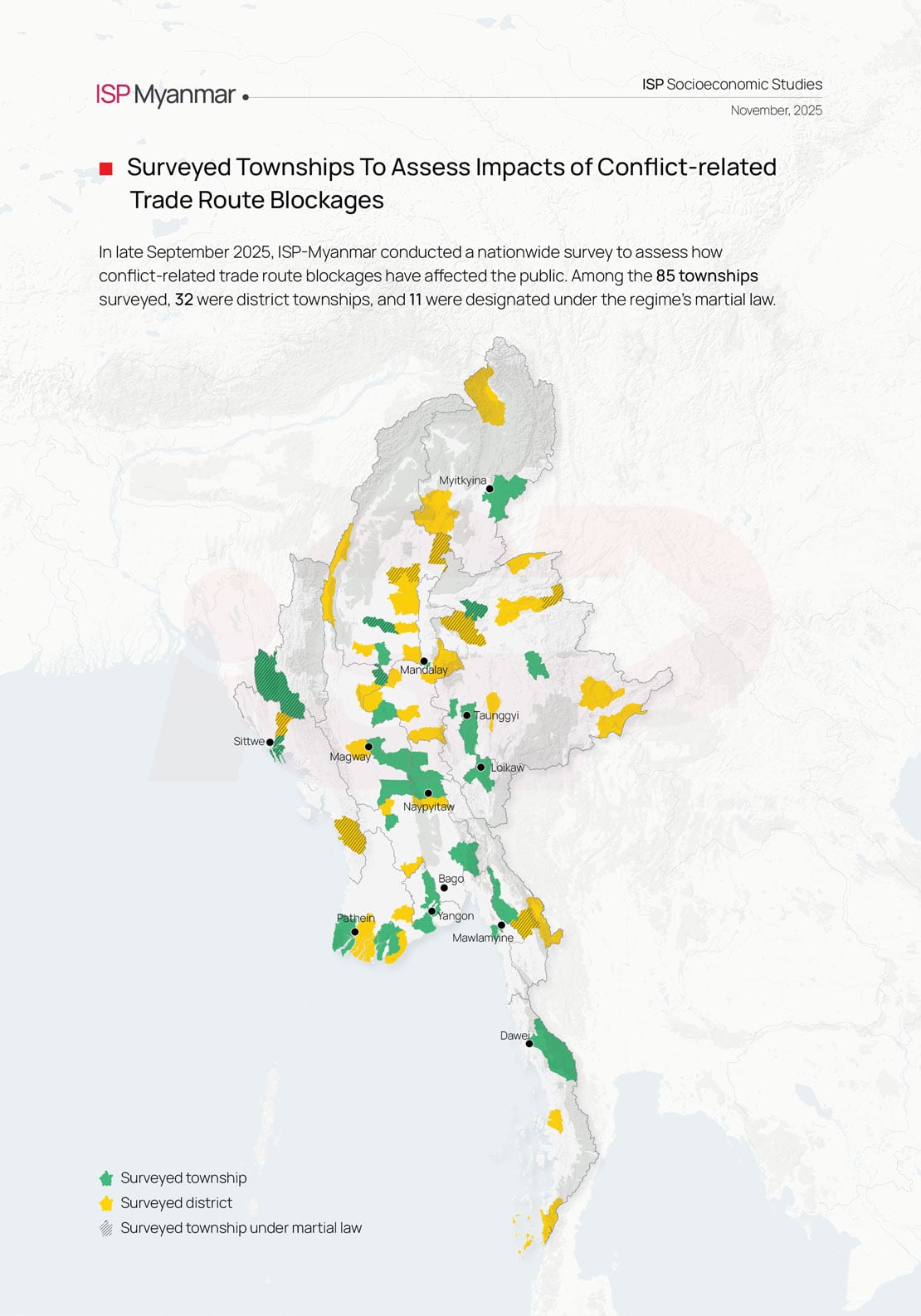

In late September 2025, ISP-Myanmar conducted a nationwide survey to assess how conflict-related trade disruptions have affected the public. A total of 1,015 respondents from 85 townships across all 15 regions and states of Myanmar, including the Naypyitaw Council Territory, participated in the study.

Survey findings reveal that trade disruptions have caused shortages of daily consumer goods and basic medicines, and prices for these goods have increased by one and a half to twice, or even three or four times, in some areas. The healthcare sector has been hit hard, particularly due to medicine shortages, price surges, and difficult access to healthcare facilities. Livelihoods have also deteriorated, forcing many to switch jobs or struggle with more restricted income. To cope, people have turned inward—cutting back on household budgets, consumption, and relying on support from local charity groups and Civil Society Organizations (CSOs) to get by.

The report finds that the State Security and Peace Commission (SSPC)’s mismanaged economic policies and administration have upended much of the country’s economic system. Survey results also suggest that the SSPC’s administrative apparatus has limited capacity to provide relief and promote wellbeing of the citizens. Similarly, the ability of Ethnic Armed Organizations (EAOs), local defense forces (PDFs and LPDFs), and the National Unity Government (NUG) to offer meaningful assistance remains severely limited as alternative service providers.

Respondents felt that they do not have enough for their needs compared to last year citing rising prices and poor job prospects. As conditions continue to worsen, the public’s foremost demands are for employment and personal security. When asked how they viewed current conditions, just over half of respondents said they “can continue to struggle on,” while a significant portion also described the situation as “hopeless.” Only a small minority believed conditions “will get better.”

The survey findings are organized into five sections. These findings are preliminary rather than conclusive, underscoring the need for more comprehensive socioeconomic research. Some of the results were also discussed in the October 18, 2025, episode of 30 Minutes with the ISP, titled “The Spirit Is Willing, but the Flesh Is Weak.” The full discussion, with English subtitles, is available on ISP-Myanmar’s website and YouTube channel.

1. Commodity Shortages and Price Surge

In the 60 days leading up to September 23, 2025, a vast majority of respondents—85 percent (863 respondents)—reported shortages of imported goods caused by trade blockages (see Figure 1).

The most common shortages were everyday consumer goods. Medicine shortages were the second most common, followed by dry food, basic food items and personal hygiene products. 66 percent (674 respondents)reported shortages of consumer goods, while 61 percent (620 respondents)cited shortages of basic medicines. Only three percent (36 respondents)said they had experienced no shortages (see Figure 2).

Rising prices compounded these problems; 48 percent (486 respondents)said prices had increased by 1.5 times, while 40 percent (403 respondents) said prices had doubled. Another seven percent (68 respondents) and two percent (22 respondents), respectively, reported that prices had risen threefold and fourfold. Only three percent (36 respondents) said they had seen no price increase at all (see Figure 3).

Among the 979 respondents who answered that prices had increased, when they were asked which goods had become more expensive, 79 percent (over 770 respondents) pointed to daily consumer items and basic foodstuffs while 73 percent (710 respondents) to basic medicines (see Figure 4).

Unsurprisingly, 92 percent (938 respondents) said these developments had directly affected their families and themselves, while eight percent (77 respondents) reported no impact (see Figure 5).

Market conditions have also deteriorated. Half of respondents (510 people) said it had become slightly harder to purchase goods for their households over the past 60 days, and 25 percent (250 respondents) said conditions had “noticeably worsened.” A further 23 percent (235 respondents) reported no change, while 1.8 percent (18 respondents) said the situation had improved, and only 0.2 percent (two respondents) found that conditions were notably improved (see Figure 6).

2. Impacts on the Healthcare

The healthcare sector has been hit hard by the crisis, leading to shortages and price hikes of medicines. Furthermore, there have been difficulties in visiting hospitals or clinics and in purchasing medicines or medical supplies.

In the past 60 days, 74 percent (749 respondents) reported difficulties in purchasing medicines or medical supplies (see Figure 7), primarily due to sharp price increases (see Figure 8).

While 60 percent (606 respondents) said they could still reach hospitals or clinics without major difficulty, 27 percent (270 respondents) found it hard to do so, 10 percent (107 respondents) could only go occasionally, and three percent (32 respondents) said they could not go at all (see Figure 9).

3. Impacts on Livelihoods

The conflict-driven disruptions along trade routes have also affected the livelihoods of the respondents and their households. When asked whether there had been changes to their job or livelihood within 60 days before September 23, 2025, 36 percent (365 respondents) reported that they or their family members had experienced such a change, while the other 64 percent (650 respondents) had not (see Figure 10).

When asked whether their income had changed, 34 percent (344 respondents) reported no change. Meanwhile, 35 percent (360 respondents)reported a slight decrease, and 29 percent (290 respondents) reported a significant decrease. In contrast, a very small percentage of respondents experienced an income increase: only 1.5 percent (16 respondents) saw a raise, and an even smaller 0.5 percent (five respondents) reported a significant increase (see Figure 11).

4. Daily Struggles and Coping Mechanisms

The combination of a declining economy and ongoing armed conflicts has exacerbated the population's socioeconomic crisis. In response to the crisis—characterized by insufficient income, commodity shortages, and price hikes—respondents primarily adopted some coping strategies: 76 percent (775 respondents) reported cutting back, and a very similar 75 percent (766 respondents) stated they only purchase cheaper goods and food. More than half — 52 percent (525 respondents) — are also reducing their meat and fish consumption. Other coping strategies include borrowing money, pawning possessions, and eating one less meal a day (see Figure 12).

Inquiring into the social impact of the economic crisis, the survey found that 81 percent (822 respondents) reported a widespread increase in theft, burglary, and fraud, alongside a pervasive rise in anxiety and worry by 80 percent (811 respondents). The crisis has spurred an increase in migration, reported by 68 percent (694 respondents), and a rise in people engaging in illegal work, reported by 44 percent (447 respondents). Alarmingly, a rise in domestic violence was reported by 31 percent (312 respondents); an increase in robbery was observed by 24 percent (243 respondents); and, most distressingly, an increase in suicide within the community was reported by seven percent (74 individuals) (see Figure 13).

5. Capacity for Support and Hope

When asked who was providing assistance amid these hardships, nearly half of the respondents—49 percent (496 people)—gave a stark answer: “no help at all.” The next most common response is the "mutual help between locals", answered by 37 percent (376 respondents). Moreover, 28 percent (285 respondents) and 26 percent (269 respondents)reported the support of local charity groups and civil society organizations, respectively. In sharp contrast, institutional help was reported as minimal. The SSPC’s administrative capacity to provide support is seen as minimal, while that of EAOs, local defense forces (PDFs and LPDFs), and the NUG remains limited (see Figure 14).

Inquiring the question of whether the respondent and the family feel a sense of financial security in 2025 compared to 2024, a striking majority — 89 percent (899 respondents) —said they do not (see Figure 15).

When asked to explain their responses, the respondents cited price increases and an unstable economy (see Figure 16).

When asked about the most urgent need amid these immediate pressures, the top answer was job opportunities, with 80 percent (817 respondents). The second most critical need, indicated by 64 percent (647 respondents), was security, followed by healthcare services as the third pressing need, at 57 percent (574 respondents). Over half (more than 500 respondents) cited food and transportation as an urgent need. Education was cited by the relatively smallest proportion of respondents, at 35 percent (355 respondents) (see Figure 17).

At the end of the survey, when summarizing their views about the ongoing situations, 53 percent (539 respondents) reported that they can continue to struggle on. However, 42 percent (424 respondents) believe the situation is hopeless, while only five percent (52 respondents) expressed optimism, saying things will get better (see Figure 18).

Respondent Demographics

A total of 1,015 respondents participated in the survey. 57 percent were female (579 respondents), followed by 41 percent male (417 respondents), and two percent others (19 respondents). The survey covered a mix of locations: urban areas, rural areas, border areas, and IDP (Internally Displaced Person) camps. Participants were 18 years of age and older, with the 26–40 age group the largest, followed by those aged 41–60. In terms of monthly household income, 24 percent reported earning between 400,000 and 600,000 MMK, 20 percent between 200,000 and 400,000 MMK, and 18 percent over 1 million MMK.

Survey Methodology

This brief survey was conducted to examine the impact of conflict-related trade blockades on the public. A total of 1,015 respondents from 85 townships across all 15 regions and states of Myanmar, including the Naypyitaw Council Territory, participated in the study.

A quantitative approach was used in the data-collection. A sampling frame was created for a sample population targeting 1,020 people across 85 townships (12 locals per township). Among these townships, 32 district-level townships and 11 townships under martial law were included, but due to communication difficulties, only 1,015 responses were received.

Purposive sampling was employed, with each township’s sample required to meet four criteria:

- respondents must be local residents of the township

- include at least five women

- must reside in one of the area types: urban, rural, border, and IDP camp residents

- be aged 18 or older

Data was collected via online surveys, phone calls, and in-person interviews from September 23-28, 2025.

The survey was conducted by the respective research team leaders in accordance with the ISP-Myanmar's security protocols and ethical guidelines. During the interview, respondents were informed and consented to the secure collection of their personal information and responses in accordance with the ISP-Myanmar’s data security policies. Upon completion of the survey, the data collector stores the collected data in accordance with ISP-Myanmar's established protocols.

Please find other research and publications here.

Download the publication here.